Varun Beverages Q2 2025: Navigating Growth Amid Competitive Headwinds

India’s largest PepsiCo franchisee delivers resilient performance with 5% profit growth despite market challenges

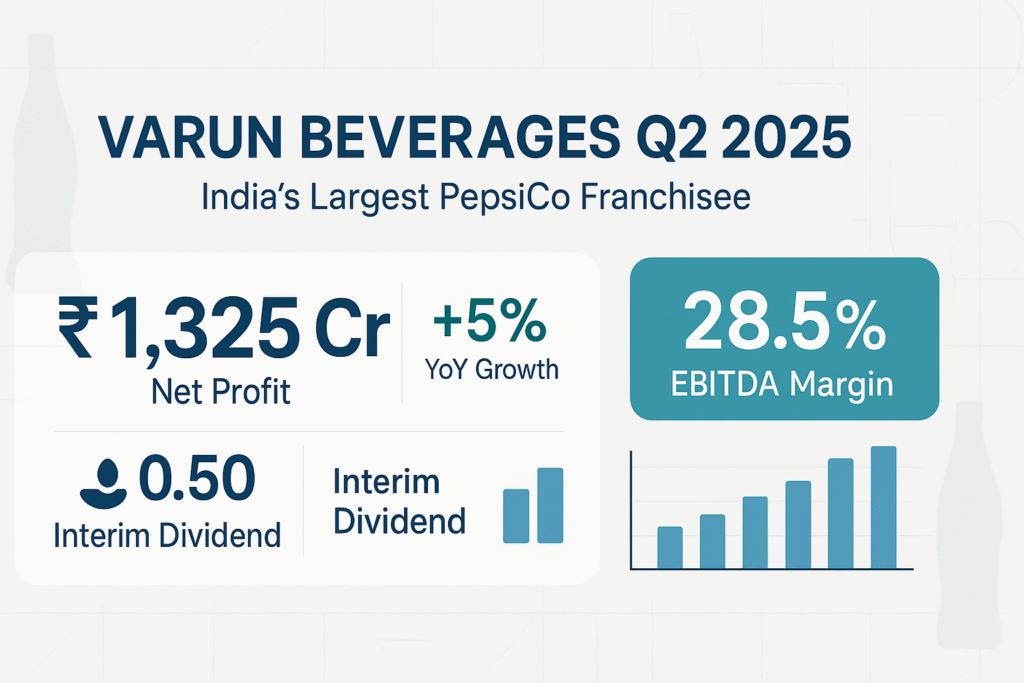

₹1,325

Crore Net Profit

+5%

YoY Growth

₹0.50

Interim Dividend

28.5%

EBITDA Margin

Executive Summary

Varun Beverages Limited (VBL) demonstrated remarkable resilience in Q2 2025, delivering 5% net profit growth to ₹1,325.49 crore despite facing unprecedented challenges from unseasonal weather patterns and intensifying competition. The company’s ability to maintain EBITDA margins at 28.5% while absorbing a 3% volume decline showcases exceptional operational efficiency and strategic positioning in India’s dynamic beverage market.

Key Highlight

VBL achieved profit growth while revenues contracted 2.5%, demonstrating strong pricing power and cost discipline that positions the company well for recovery as market conditions normalize.

Q2 2025 Performance Metrics

Company Profile & Market Dominance

Varun Beverages Limited stands as India’s largest PepsiCo franchisee and the second-largest globally outside the United States, serving approximately one-fifth of the world’s population through its extensive bottling and distribution network.

VBL At A Glance

37

Manufacturing Facilities

2,500+

Distribution Depots

1M+

Retail Outlets Served

90%

PepsiCo India Operations

| Geographic Segment | Facilities | Market Position | Growth Rate |

|---|---|---|---|

| India | 31 Plants | Market Leader | -7.1% |

| International | 6 Plants | Expanding | +15.1% |

| Africa | 4 Countries | Strategic Focus | +20%+ |

Financial Performance Analysis

The 5% net profit growth to ₹1,325.49 crore should be viewed as remarkably resilient given the extraordinary headwinds facing India’s beverage industry in Q2 2025. Unseasonal early monsoons during peak summer months severely disrupted the critical April-June selling season.

Revenue vs Profit Trend (Last 5 Quarters)

| Financial Metric | Q2 2025 | Q2 2024 | Change | Analysis |

|---|---|---|---|---|

| Revenue | ₹7,017 Cr | ₹7,193 Cr | -2.5% | Weather Impact |

| Net Profit | ₹1,325 Cr | ₹1,262 Cr | +5.0% | Cost Optimization |

| EBITDA Margin | 28.5% | 27.7% | +0.8pp | Efficiency Gains |

| Volume Growth | -3.0% | +12% | -15pp | Monsoon Effect |

Dividend Policy Evolution

The ₹0.50 interim dividend represents VBL’s shift toward more frequent shareholder distributions, marking the second interim payment for FY2025. This evolution demonstrates enhanced shareholder engagement while maintaining conservative payout ratios.

Dividend History & Payout Evolution

*2025 includes two interim dividends of ₹0.50 each

| Year | Dividend Per Share | Payout Ratio | Dividend Yield | Growth Rate |

|---|---|---|---|---|

| 2021 | ₹2.50 | 12.5% | 0.8% | – |

| 2022 | ₹3.00 | 13.2% | 0.9% | +20% |

| 2023 | ₹4.00 | 14.1% | 1.1% | +33% |

| 2024 | ₹5.25 | 15.8% | 1.2% | +31% |

| 2025 (YTD) | ₹1.00* | 10.5% | 0.2% | On Track |

Market Position & Competitive Dynamics

VBL’s stock has faced significant headwinds in 2024-2025, declining approximately 30% from peak levels despite strong operational fundamentals. The market concerns primarily stem from competitive pressure from Reliance’s Campa Cola rather than operational performance.

Market Share Analysis – Indian Beverage Industry

35%

VBL (PepsiCo)

40%

Coca-Cola India

15%

Regional Players

10%

Others/New Entrants

Campa Cola Challenge

Reliance’s aggressive pricing strategy offers 200ml bottles at ₹10 versus ₹20 for PepsiCo/Coca-Cola products, creating market share concerns. However, VBL’s extensive distribution network of one million visicoolers and rural penetration provide significant competitive advantages.

Competitive Landscape Analysis

The Indian beverage market is experiencing a transformation with new entrants challenging established players. VBL’s response strategy focuses on operational efficiency, product innovation, and leveraging its distribution strengths.

| Competitor | Market Strategy | Pricing | Distribution | VBL Advantage |

|---|---|---|---|---|

| Coca-Cola India | Premium Positioning | Premium | Extensive | Better Margins |

| Campa Cola (Reliance) | Value Pricing | Aggressive | Growing | Established Network |

| Regional Players | Local Focus | Competitive | Limited | Scale & Branding |

| International Brands | Innovation | Premium | Urban Focused | Rural Penetration |

VBL Competitive Advantages

2039

PepsiCo Franchise Until

1M+

Visicoolers Installed

90%

Backward Integration

6

International Markets

Strategic Outlook & Investment Thesis

VBL’s strategic positioning for long-term growth remains robust despite short-term challenges. The company’s net cash position of ₹2,524 crore provides financial flexibility for expansion and acquisitions.

Growth Drivers & Strategic Initiatives

Rural Expansion

Penetrating untapped rural markets with significant growth potential

International Growth

Expanding African operations contributing 17% of revenues

Product Diversification

Entry into snacks and dairy segments

Technology Integration

₹200 crore Lunarmech acquisition for automation

| Investment Metric | Current Status | Target/Outlook | Timeline |

|---|---|---|---|

| Stock Price | ₹486-487 | ₹618 (Avg Target) | 12-18 months |

| Market Cap | ₹1,64,581 Cr | Growth Expected | Long-term |

| Dividend Yield | 0.2-0.5% | Growing Payouts | Annual |

| CAPEX Investment | ₹3,600 Cr Planned | Capacity Expansion | 2025-2027 |

Frequently Asked Questions

What caused VBL’s volume decline in Q2 2025?

▼

Unseasonal early monsoons during peak summer months severely disrupted the critical April-June selling season. May 2025 received 85.7% more rainfall than usual, impacting the beverage consumption patterns that typically drive 50% of annual volumes.

How significant is the Campa Cola threat to VBL?

▼

While Campa Cola’s aggressive pricing (₹10 vs ₹20 for equivalent products) creates market pressure, VBL’s extensive distribution network of one million visicoolers and deep rural penetration provide significant competitive advantages. The impact is expected to be limited given Campa’s nascent distribution capabilities.

Is VBL’s dividend sustainable given current challenges?

▼

Yes, VBL maintains conservative payout ratios (averaging 14.67%) and has transitioned to a net cash position of ₹2,524 crore. The ₹0.50 interim dividend represents manageable 13-15% of profits while preserving capital for growth investments.

What are VBL’s key growth drivers for the future?

▼

Key growth drivers include rural market expansion, international operations (particularly Africa contributing 17% of revenues), product diversification into snacks and dairy, and technology integration through the ₹200 crore Lunarmech acquisition.

How does VBL compare to other beverage companies?

▼

VBL is India’s largest PepsiCo franchisee and second-largest globally outside the US. It commands 90% of PepsiCo’s India operations and holds approximately 35% share of India’s organized beverage market, with superior margins and distribution reach compared to competitors.

What is the analyst consensus on VBL stock?

▼

Despite near-term pressures, analyst consensus remains positive with average target price of ₹618 (27% upside potential). Goldman Sachs, HSBC, and Jefferies maintain Buy ratings, viewing current valuations as attractive given VBL’s structural advantages and long-term growth prospects.

Key Takeaways

✓ Operational Excellence

5% profit growth despite 3% volume decline demonstrates strong cost discipline and pricing power.

✓ Financial Strength

Net cash position of ₹2,524 crore provides flexibility for growth investments and acquisitions.

⚠ Near-term Challenges

Weather disruptions and competitive pressure from Campa Cola creating temporary headwinds.

📈 Long-term Outlook

Structural advantages and growth initiatives position VBL well for sustained value creation.

Stay Updated on VBL Performance

Get the latest analysis and insights on Varun Beverages and other top Indian stocks

Subscribe to UpdatesGNG Electronics: Big Share IPO Allotment Status & Key Insights.

Post Comment